US firms secure some of the biggest disputes in London

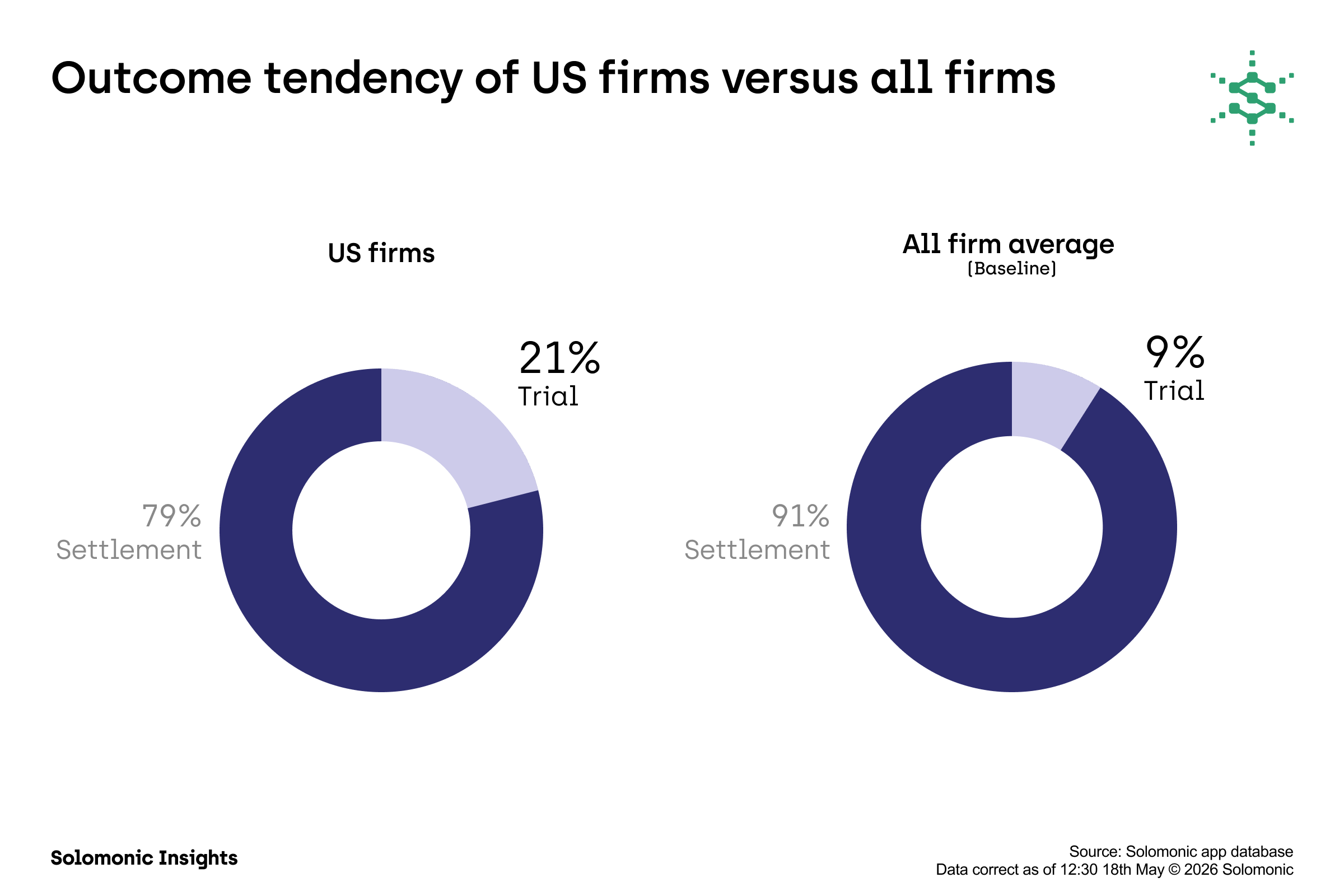

£10m median claim value – 13x higher than the overall median. 21% trial rate vs 9%. US firms are securing many of the biggest, most complex disputes in London.

For more than a decade, the narrative around the London disputes market has been one of relentless US expansion. Aggressive lateral hiring, eye-watering pay and rapid office growth have signalled a sustained and deliberate investment into London litigation. The question has been whether that investment is paying off?

Solomonic court data reveals where that investment is having an impact.

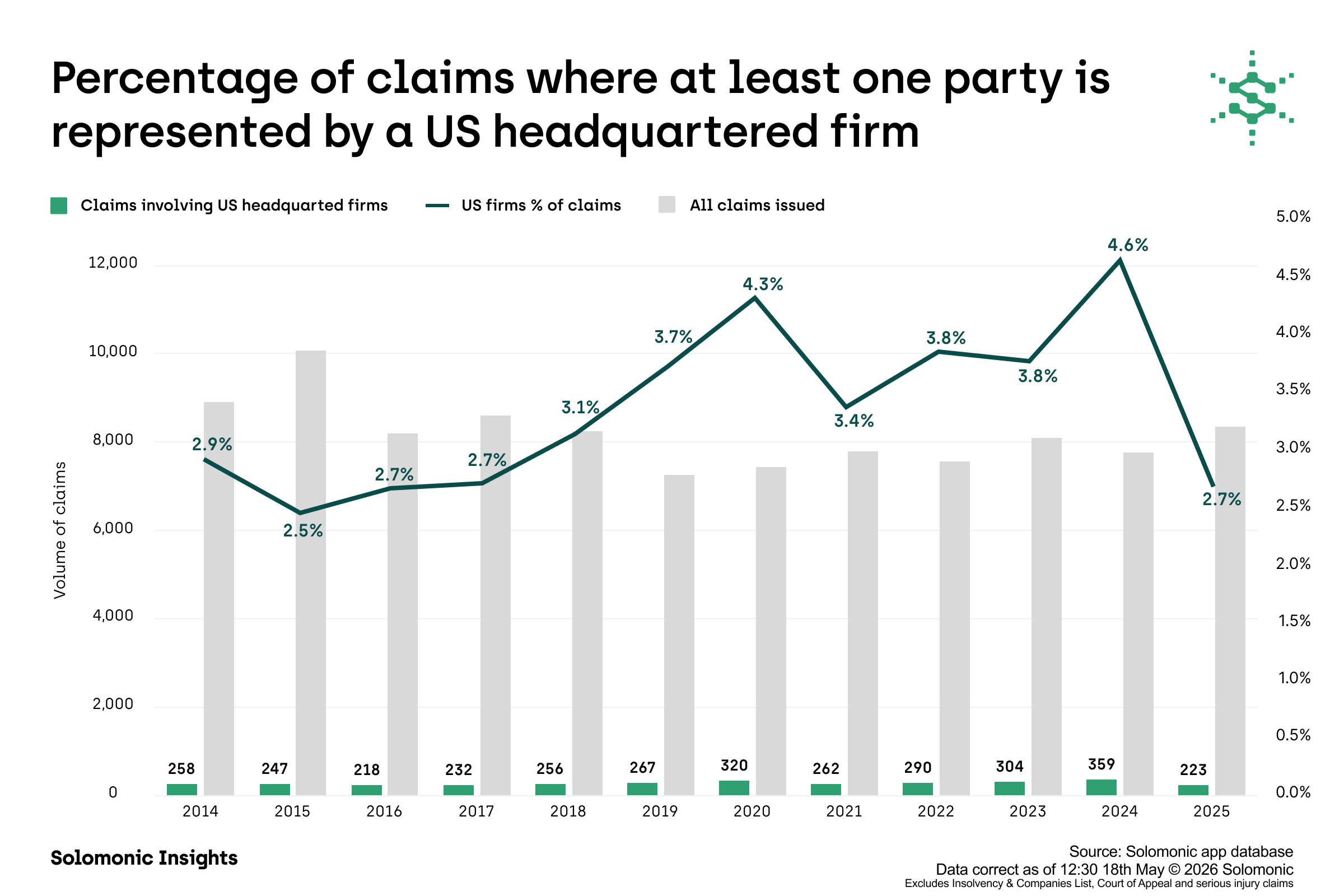

Percentage and volume of claims where at least one party is represented by a US headquartered firm

Solomonic data shows that US firms have deliberately concentrated their efforts at the very top of the market. While they account for around 4% of all claims by volume (2020 to 2025) – the quality and scale of the work they are winning is notable.

The median claim value for US firms in 2025 stood at approximately £10 million, compared to an all firm average of just £740,000. That is a 13x gap. US firms are not competing across the full spectrum of London litigation; they are positioning themselves at its most valuable and consequential end.

That strategic positioning is also reflected in trial rates. Claims involving US firms reached a judicial outcome 21% of the time, compared to a 9% average for all claims. As a segment, US firms are disproportionately involved in the most hard-fought, high-stakes disputes, the cases that go the distance.

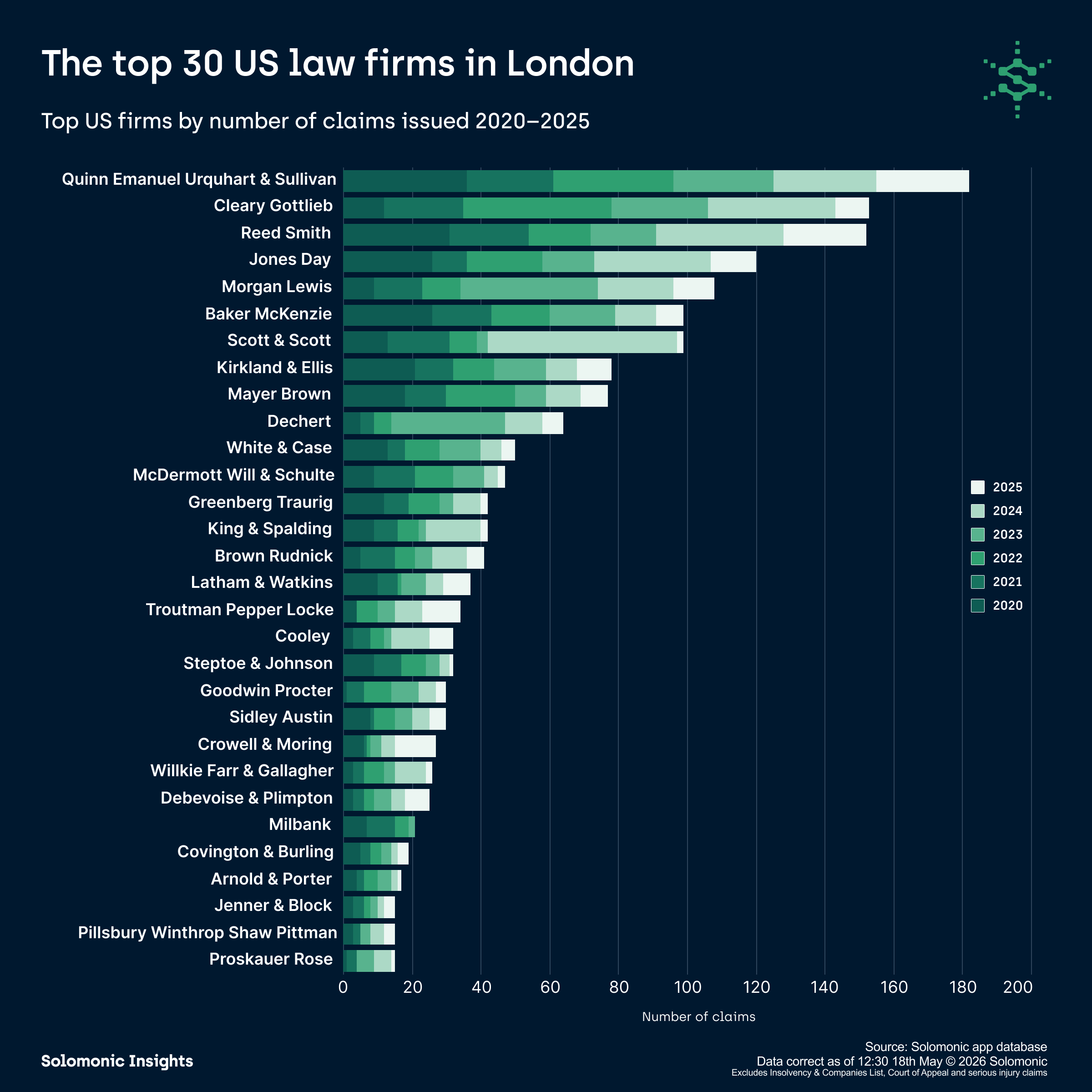

Top US law firms in London

A handful of US firms stand out for their sustained volume of disputes in the English High Court.

Top US firms by number of claims issued 2020–2025

Between 2020 and 2025, the most active US firms by claim count were Quinn Emanuel Urquhart & Sullivan, Cleary Gottlieb Steen & Hamilton, Reed Smith, Jones Day and Morgan, Lewis & Bockius. Each was involved in more than 100 claims over the six-year period.

Close behind are Baker McKenzie and Scott & Scott, both involved in 99 claims.

US firms have evidently established themselves as a go-to choice for the most complex, highest-value and most trial-intensive disputes in London.

Almost one in five cases in the Commercial Court now involves a US firm

The clearest sign of US firms increasing their influence emerges when looking beyond volume and focusing instead on where they are litigating.

US firms in the Commercial Court

The Commercial Court, the apex forum for high-value, complex business litigation in England and Wales, shows an upward trend in US firm involvement in recent years.

US firms accounted for an average of 15.9% of Commercial Court claims between 2014–2019; 15.5% between 2020–2022; and 18.9% between 2023–2025. In other words, almost one in five cases before the Commercial Court now involves a US firm.

While US firms may still represent a relatively small proportion of the overall litigation market, they are increasingly concentrated in the complex disputes that matter most financially.

Beyond the Commercial Court, US firms are also particularly active in the Business List; the General King’s Bench Division; the Intellectual Property List; the Competition Appeal Tribunal; and the Technology and Construction Court.

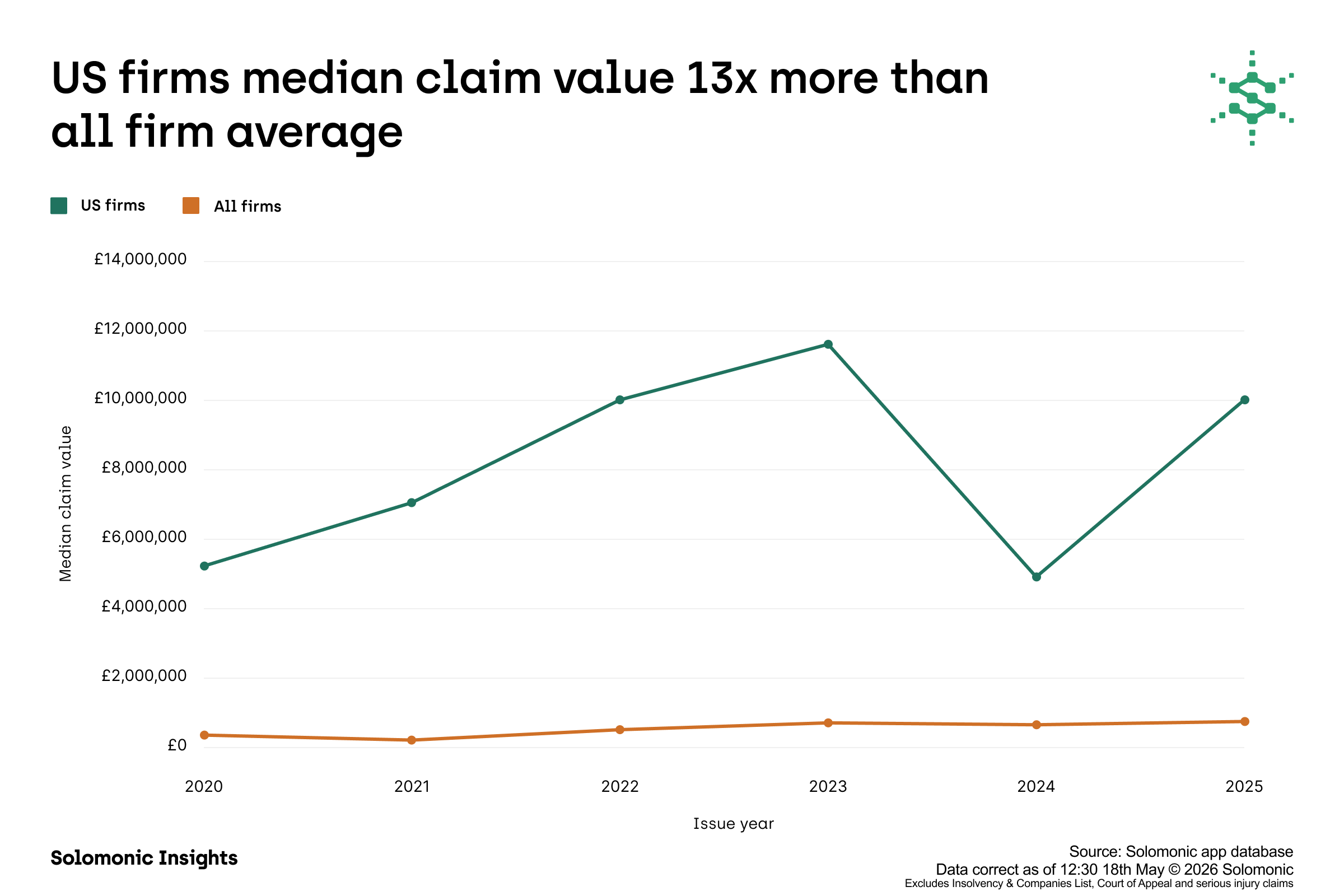

Following the money

US firms are not just present in high-value disputes – they have concentrated their practices in higher value litigation.

US firms median claim value 13x more than all firm average

In 2025, the median claim value for US firms stood at approximately £10 million, compared to an all firm average of around £740,000 – a 13x gap.

The highest value cases involving US firms

The highest value disputes involving US law firms in England & Wales reveal a litigation landscape shaped less by conventional commercial claims and more by global high-stakes disputes.

At the top end, value is concentrated in mass group litigation, competition collective actions and sovereign or arbitration-related disputes. The £36bn BHP dam proceedings exemplify the scale achievable through large claimant cohorts, while cases such as Merricks v Mastercard highlight the impact of opt-out competition claims capable of generating multi‑billion-pound valuations.

In parallel, disputes such as Nigeria v P&ID and Law Debenture v Ukraine demonstrate how arbitration awards and sovereign debt exposures continue to produce some of the largest claims before the English courts.

These disputes are not evenly distributed across the court system. Instead, they are channelled through specialist forums, reflecting the increasing procedural sophistication required to manage high-value, multi-party claims.

Quinn Emanuel Urquhart & Sullivan stands out acting on either side of complex, high-stakes litigation. Covington & Burling and Willkie Farr & Gallagher are heavily present in competition and consumer collective proceedings.

US firms are not just present – they are embedded in some of the most complex, cross‑border and highest-value dispute categories, with clear specialisation emerging by dispute type (competition, arbitration, enforcement).

| # | Claim number | Claim title | Value sought | US firm(s) |

|---|---|---|---|---|

| 1 | HT-2022-000304; HT-2023-000058 | Municipio de Mariana, Rodovia Juscelino Kubitschek and others v BHP Group Limited and another; Município de Coronel Fabriciano and Others v BHP Group (UK) Ltd and another | £36bn | White & Case (Part 20) |

| 2 | 1266/7/7/16 | Walter Hugh Merricks CBE v Mastercard Incorporated and Others | At least £14bn |

Quinn Emanuel Urquhart & Sullivan (Claimant) Willkie Farr & Gallagher (Claimant) Jones Day (Defendant) Milbank (Defendant) |

| 3 | CL-2023-000401 | Magomedov and others v. TPG Group Holdings (SBS), LP and others | US$15.9bn |

Curtis, Mallet-Prevost, Colt & Mosle (Defendant) Quinn Emanuel Urquhart & Sullivan (Defendant) |

| 4 | CL-2018-000182; CL-2019-000752 | Process & Industrial Developments Ltd v The Federal Republic of Nigeria; Federal Republic of Nigeria v Process & Industrial Development Ltd | US$11bn | Quinn Emanuel Urquhart & Sullivan (Claimant; Defendant) |

| 5 | 1749/7/7/25 | Association of Consumer Support Organisations Ltd v (1) Amazon.com, Inc., (2) Amazon Europe Core S.À.R.L., (3) Amazon EU S.À.R.L, (4) Amazon U.K. Services Ltd., and (5) Amazon Payments U.K. Limited | Between £3.6bn and £7.5bn | Covington & Burling (Defendant) |

| 6 | BL-2024-MAN-000048 | Swifthold Foundation v Fast International Trading Group and another | At least US$5.9bn | Boies Schiller Flexner (Claimant) |

| 7 | BL-2022-002097 | NMC Health Plc (in administration) v Shetty and others | US$4bn |

Quinn Emanuel Urquhart & Sullivan (Claimant) Baker McKenzie (Defendant) |

| 8 | 1689/7/7/24 | Consumers' Association ("Which?") v Apple Inc, Apple Distribution International Limited, Apple Europe Limited & Apple Retail UK Limited | Between £2bn and £2.8bn |

Willkie Farr & Gallagher (Claimant) Covington & Burling (Defendant) |

| 9 | 1644/7/7/24 | Professor Andreas Stephan v Amazon.com Inc. & Others | Up to £2.7bn | Covington & Burling (Defendant) |

| 10 | FL-2016-000002 | The Law Debenture Trust Corporation PLC v Ukraine, Represented By the Minister of Finance of Ukraine Acting Upon the Instructions of the Cabinet of Ministers of Ukraine | US$3bn | Quinn Emanuel Urquhart & Sullivan (Defendant) |

Are US firms more willing to go the distance?

US firms are perceived as more aggressive litigators, particularly given their reputation in the US market and their growing involvement in funded disputes, class actions and competition claims.

Between 2020 and 2025, 51% of US firms’ involvements were on the claimant side and 49% on the defendant side. Across all firms, claimant-side involvements accounted for 55% of the total, 45% on the defendant side.

The most striking difference between US firms and the wider market emerges when looking at judicial outcomes. Collectively, US firms are significantly more likely to take claims all the way to trial.

Outcome tendency of US firms versus all firms

Claims involving US firms reached a judicial outcome 21% of the time, compared to just 9% for all firms. Conversely, US firm cases settled 79% of the time, compared to 91% for other firms.

The figures suggest that US firms are disproportionately involved in the most hard-fought, high-stakes disputes. Whether that reflects client profile, litigation strategy, case selection or practice focus, it points to a requirement for issue to trial case strategy and management capabilities.

The bigger picture

The data confirms that US firms have executed a high-value, high-complexity strategy in the English jurisdiction that has reshaped the market.

US firms have not sought to compete across the full breadth of English litigation – they have targeted the most financially and strategically significant disputes.

US firms have established themselves at the premium end of the market: higher-value disputes, more complex litigation, stronger trial exposure and a growing footprint in the Commercial Court and competition sphere.

If you would like to learn more about Solomonic’s award-winning litigation data and analytics, trusted by more than 10,000 practitioners and 60% of the UK’s top 50 litigation firms, please get in touch with us at info@solomonic.co.uk for a confidential introduction to the platform.

‘US law firm’ defined as a US-based firm that has opened an office in London (not a London firm merged with a US firm)*

Analysis excludes Insolvency & Companies List, Court of Appeal, Asbestos List, Clinical Negligence and Personal Injury claims

*With thanks to RPC for assistance on compiling the list of 66 US headquartered firms (correct as of April 2026).