The next wave of war risk claims: Insights from litigation data

Could a new range of war risk policy claims be on the horizon following the current conflict in the Middle East?

The current crisis in the Middle East has unsurprisingly raised concerns about the conflict’s long-term consequences. Global energy markets are already reacting, with prices climbing rapidly, mirroring the surge seen after Russia’s full-scale invasion of Ukraine in early 2022.

The Russo-Ukrainian war had significant implications for the insurance industry, generating a wave of high-value claims that dominated headlines and exposed the complex legal consequences. If hostilities involving Iran continue to intensify and spread, the insurance sector could face a similar, if not broader, uptick in claims, particularly given the centrality of energy infrastructure and maritime transport to the current crisis.

The insurance sector has always played a significant role in times of conflict, with war risk insurance providing specialised cover for damage caused by acts of war. However, such coverage is rarely straightforward in practice. Disputes often arise around policy interpretation, causation and the extent of insured losses.

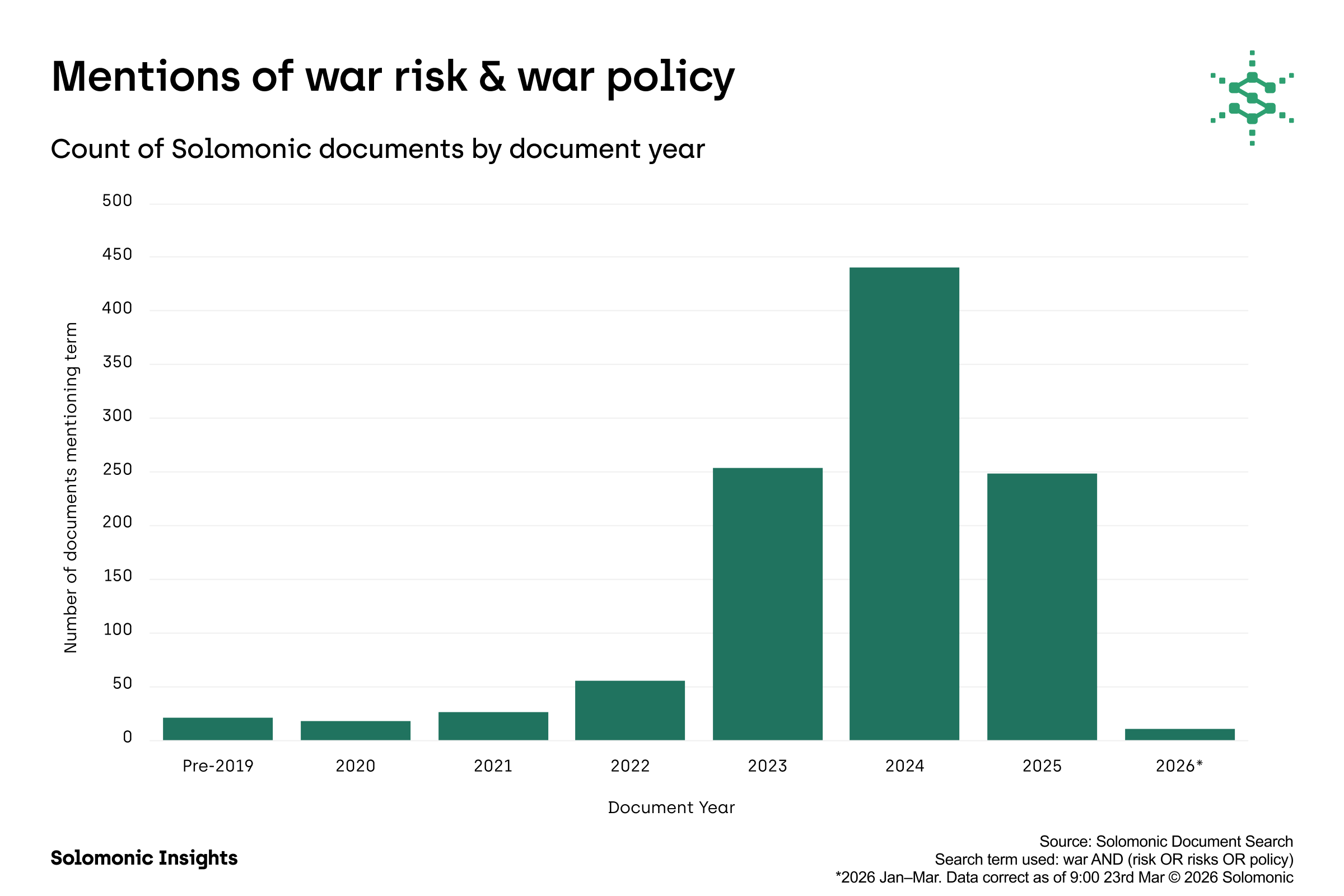

Using the Solomonic Document Search tool, we analysed how frequently “war risk/policy” has been mentioned in High Court documents over recent years. Since 2020, the term has appeared in over a thousand documents, with mentions peaking in 2024 (440). The war in Ukraine began in 2022 and the sharp rise in mentions over the following years mirrors the wave of claims filed during that period, highlighting how large-scale geopolitical events translate into sustained litigation activity.

We asked partners Fiona Treanor and Alexander Oddy, and senior associate Joanna Giza at Herbert Smith Freehills Kramer LLP to share their thoughts on the recent developments:

"As tensions rise in the Middle East, commercial contracts will come under pressure. Parties may need to issue force majeure notices or rely on material adverse change (MAC) clauses across supply and shipping contracts. War exclusions will come under scrutiny, particularly where hostilities have indirectly impacted contractual performance.

Supply chain dislocation will take time to unravel with an increased risk of insolvencies and credit risk defaults, particularly as freight and oil prices rise. Both commercial and insurance claims will likely follow as incentives to exit or renegotiate contracts grow.

From an insurance-specific perspective, property damage claims affecting both maritime and land‑based assets can be expected across multiple locations and jurisdictions along with business interruption and event cancellation claims, all subject to any war risk exclusions.

Unlike the Russian aircraft insurance claims, insurance losses are unlikely to be homogeneous. Instead, a piecemeal pattern of claims is more likely, raising aggregation questions for reinsurers.

War risk insurers are reportedly cancelling cover or seeking higher premiums. The lessons from the Russian aviation claims include the need for scrutiny of notices of cancellation, particularly where the insured may be in the "grip of the peril".

Overall, it remains to be seen how many disputes reach the English courts, given many commercial contracts, insurance and reinsurance policies contain arbitration clauses."

If you would like to learn more about Solomonic’s leading data and analytics, please get in touch for a confidential introduction to the platform.